For 50 years, the CENTURY 21 network has thrived from the presence of different perspectives and continues to provide opportunities and a sense of belonging for every individual and company that affiliates with the brand. It is this long-standing culture of diversity, equity, and inclusion that is the CENTURY 21 competitive advantage.

At CENTURY 21 Real Estate Alliance Group, we are incredibly proud to celebrate inclusivity and diversity within our team and among our clients. We recognize the importance of representing a broad range of individuals and are committed to providing extraordinary experiences for all.

As one of the most diverse populations in California, we are thrilled to serve everyone who wants to sell real estate. No matter who you are, we’ve got you covered.

Our global expansiveness with approximately 14,000 bureaux in 85 countries and a global network of extraordinary sales associates allows us to help clients from all over the world. While regionally CENTURY 21 Real Estate Alliance Group’s 35+ locations across the state of California represents a beautiful melting pot of diversity with over 46 languages spoken. Earning CENTURY 21 Real Estate Alliance Group the honor of receiving the Marsh Fisher Diversity Award, which recognizes our commitment to cultural diversity and improving minority homeownership.

Michael Miedler, President, and CEO of CENTURY 21 Real Estate, reflects on our journey, saying, “We’re proud to have a workforce and franchise base that is as diverse as the people we serve every day. We are committed to continuing that cultural legacy for the next 50 years as a global real estate franchise leader. It’s a mission that is central to our strategy of providing extraordinary experiences and remaining a domicile where all those we touch can thrive.”

Orhan Tolu, President of CENTURY 21 Real Estate Alliance Group, regularly states, “It doesn’t matter where you come from, but rather where you are going that matters.”

We are honored to be a part of CENTURY 21 and CENTURY 21 Real Estate Alliance Group, where inclusivity and diversity are celebrated, and every individual is welcomed with open arms. Come join us and let us help you achieve your real estate goals.

2023 began with an uptick in the sale of new homes but the driving force in the housing market continues to be acheteurs backing out of contracts. January sales were down 26% compared to a year ago. The national cancellation rate is now à propos de 20%, with 1 in 5 contracts ending. In fact, KB Homes, one of the largest builders in the country reported 68% of its orders for new homes were canceled in 4th quarter of 2022.

AFFORDABILITY

Building new homes can take up to a year so the rising interest rate from 3% to 6% greatly affected the affordability of homes. Many families may no longer qualify for a hypothèque or have decided they can no longer afford the domicile they chose.

Acheteurs are also struggling to sell their current homes with the changing market. With housing prices growing slower or even falling slightly in some markets, many are having to reevaluate whether now is the best time to buy or sell.

HOMEBUYERS CHOOSIER

Affordability is not the only issue causing cancellations. House hunters now can take the time to explore their options and be choosier. During the pandemic domicile buying frenzy, acheteurs had to act quickly and take homes however they could get them often foregoing domicile inspections. Today, Acheteurs have the time to do the inspections allowing them to see any potential problems a domicile may have as well as continue their search in case a better domicile comes on the market.

PREVENTING CANCELLATIONS

Although Real Estate Agents do not have control over affordability and findings on domicile inspections, clear communication and managing expectations can go a long way in preventing cancellations.

The biggest complaint that acheteurs et vendeurs share is a lack of communication. When they do not know what is coming next, it is understandable that they can become uneasy during the process. As an agent being dedicated to clear communication with all parties including the Buyer, Acheteurs Agent, Seller, Vendeurs Agent (if you have it), Closing Attorney, Closing Assistant, Transaction Coordinator and Lender can drastically reduce the numbers of cancellations. Some real estate experts even recommend creating one group email with instructions to everyone to “reply all” so everyone is clear with the current status and next steps.

2022 was a complete à propos de face in the Real Estate Industry going from a Seller’s Market for the last decade to a Buyer’s market in just a few short months. With transactions down 15% nationally this past year, what can Agents expect going into 2023? According to Brian Buffini’s Bold Predictions along with Lawrence Yun from National Association of Realtors, serious agents can expect to survive the first half of 2023 and thrive in the third and fourth quarters. Buffini and Yun discussed the impact of Interest Rates, Median Accueil Prices and Opportunities for agents in 2023.

INTEREST RATES

Interest rates on 30 year mortgages hit a twenty year high, which saw many acheteurs retreating due to affordability. Confidence in the Real Estate Market is high, however many people are finding the higher interest rates price them out of buying a domicile. Although the median income is $50,000 nationally, it takes $85,000 in income to purchase an average starter domicile, with 35% of salary going towards mortgages.

There is a light at the end of the tunnel on interest rates. It is anticipated that the Feds will increase rates in smaller increments the first half of 2023 yet most experts agree that rates will begin to decline the second half of the year. Perhaps even as low as the 6% range. With interest rates still historically low and continued pressure from rising rent prices, demand people will to move from renting to purchasing homes. In fact, 2/3 of Millennials surveyed stated that they do plan on buying a domicile in the next few years.

With Median Accueil Prices continually increasing, homeownership is still seen as one of the best investments. U.S. Median Accueil Prices rose 73% from 2010-2020 with continual gains expected in the next few decades.

In California, Median Accueil Prices have tripled three times since the late 1970’s with the latest jump from $209,000 in 2009 to $840,000 in 2022. Jordan Levine, VP and Chief Economist for the California Association of Realtors, sites the fact California has a strong economy even after the pandemic and creates a lot of demand on housing.

OPPORTUNITIES IN 2023

After a dramatic decline of 15% in sales for 2022, the forecast for 2023 is a decrease in unit sales of 7% and domicile prices increasing 10%. Most of that decline is anticipated in the first 2 quarters of the year but primarily in larger cities with higher prices. States and areas that have seen a migration to rural areas can expect gains in 2023 and 2024 forecasts 10% growth in sales overall.

With the tougher markets in 2022 and 2023, there will be 200,000 fewer agents by year-end resulting in less competition for business pros.

What can real estate business pros do in 2023? Buffini recommends three strategies:

1. Understand and educate the changes of the market for Acheteurs et Vendeurs.

2. Put the “I” in Investment. Be part of your clients Investment Strategy.

3. Out of state, out of mind. Build your network.

For more information on how to survive and thrive, watch Brian Buffini’s Bold Predictions:

Buying a domicile is one of the largest single purchases most people will ever make. A propos de 40 percent of Americans say that domicile-buying is the most stressful event in modern life and selling an existing domicile is a large component of that anxiety. That’s why large real estate companies began programs like iBuyer to use technology to radically simplify the selling process.

iBUYING STRATEGIES

Touted as a more convenient, less costly alternative to traditional domicile-selling, iBuyer programs had been buying homes primarily in Sun Belt markets and shattering records. But with real estate powerhouses like Zillow and now Redfin closing iBuyer divisions after big losses, the future of iBuyer strategies may be in question.

iBuyer programs began back in 2013 with Opendoor, but in 2018 really gained momentum causing concern for real estate agents and brokers. But now the housing slowdown is raising new questions à propos de the future of iBuyers. With domicile prices cooling, iBuyers, or instant acheteurs, have sharply pulled back on their purchases in recent months.

CONCEPT REMAINS SMALL

In recent news, RedfinNow said November 9 that it had closed its domicile-flipping business.

Opendoor and Offerpad, the other two major iBuyers, continue to operate but have sharply pulled back, laid-off employees and offers are not as generous as they once were. For all the headlines and hype surrounding iBuying, the concept remains small. iBuyers account for less than 1 percent of all U.S. domicile sales, according to the National Association of Realtors.

TAKEAWAYS FROM iBUYING

We cannot rest on policies and procedures but explore new proactive ways of providing 121% customer service.

Second, we must continually educate the value of hiring a REALTOR®. iBuyer programs still charged 5% in service fees which is comparable to commissions paid for less personalized service.

Last, but certainly not least, we must nurture the relationships that we work so hard to create. When buying or selling a domicile, picking up the phone and calling a trusted friend who happens to be a dynamic real estate professional needs to be their first and easiest step in the process.

Written by

April Moulton

Broker of Record, C21 Hometown Realty

DRE# 01736191

A propos de Century 21 Real Estate Alliance- Century 21 Real Estate Alliance Group is the largestCentury 21 brokerage in California powered by over 1500 real estate agents working from 35 bureaux throughout California. Now offering Escrow and Lending services specializing insolutions-based lending.

With hypothèque rates hitting 7% or more, lenders and vendeurs are getting creative to keep acheteurs in the market. One answer is a 2/1 Buydown program allowing borrowers to reduce initial hypothèque payments to affordable levels.

HOW DOES A 2/1RATE BUYDOWN WORK?

Generally speaking, a buydown program is a type of financing offer to reduce your interest rates for the first two years of a hypothèque. As a buyer, your interest rate is reduced by 2% the first year and 1% the second year. By the third year, the interest rate goes back to the original interest rate that was locked in when the loan originated.

WHO PAYS FOR THE PROGRAM?

Either a homebuyer or seller can pay for a buydown. Vendeurs can offer it as a concession to homebuyers. The payment can be made in the form of hypothèque points or a lump sum deposited into an escrow account with the lender to subsidize the borrower’s reduced monthly payments.

According to lending experts interviewed by the Washington Post, Fannie Mae, Freddie Mac and the Federal Housing Administration still require the borrower to qualify for their hypothèque at the note rate, regardless of the buydown.

PROS & CONS OF A TEMPORARY BUYDOWN

A temporary buydown can benefit both vendeurs et acheteurs, but it’s most likely to occur in a buyer’s market where there are many properties available and not enough acheteurs.

For vendeurs, it enables them to move properties faster and keeps them from staying on the market too long. For acheteurs, the reduced monthly payments can help manage initial housing expenses. This can be a strategy to buy when others have backed away due to higher interest rates and inventory is more plentiful with plans to refinance if interest rates go down.

For those acheteurs planning on refinancing at a later time, using a seller concession to purchase a 2/1 buydown can result in more savings for them rather than using their own funds for a larger down payment.

In terms of cons, a 2-1 buydown does have a high upfront cost, and may only be worth it for the buyer if they can get the buydown via a seller concession. As a seller concession, the buydown becomes part of the closing costs that the seller pays to help the buyer by reducing their closing costs.

A 2-1 buydown can be beneficial for borrowers, but be sure that you educate your clients on the ins and outs before they commit. For more information on the 2/1 Buyout Program or other alternative funding options, talk to a Century 21 Real Estate Alliance agent to find a program that best meets your needs.

A propos de Century 21 Real Estate Alliance- Century 21 Real Estate Alliance Group is the largester 1500 real estate agents working from 35 bureaux throughout California. Now offering Escrow and Lending services specializing insolutions-based lending.

You can feel it in the air! Fall 2022 has arrived, bringing lower temperatures and a cooling down of the real estate market. After the blazing housing market during the pandemic, rising interest rates have cooled down the real estate frenzy. But that’s not necessarily bad news for acheteurs.

As the housing market heated up, many would-be homeowners found themselves unable to purchase due to multiple cash offers pushing winning bids too high. Now with hypothèque rates rising since January 2022 to 7.04%, prices are starting to edge down in most housing markets.

Where’s the good news you ask? According to Thersa Ghilarducci’s article “Looking to Buy a House? It’s Not the Worst Time” published in Bloomberg October 15, 2022, “Buying an asset when the price is falling is generally a good thing. Buying a domicile now when hypothèque rates are high and housing prices are falling means as hypothèque rates stabilize or even drop, your house value will more likely inflate than if prices were rapidly increasing and hypothèque rates were increasing. Rising hypothèque interest rates and a potential recession may seem like bad news, but these trends could benefit would-be domicileacheteurs by cooling demand and dropping prices further, especially if the acheteurs are confident they won’t lose their jobs and income.”

Ghilarducci further explains, “Of course, a would-be domicile buyer must consider other important criteria besides housing prices before buying a house. Other important decision factors include having at least 20% for a down payment; whether you will live in the property for more than five years; and whether your monthly payment will be lower than 30% of your gross income.”

Although purchasing a house when interest rates and inflation are higher may not be ideal, this may be the perfect opportunity to consider buying if you can afford it. Not only can you avoid the bidding war that forced many acheteurs out of the market, you can always refinance once the Fed lower interest rates which some experts predict can be as soon as in 2023.

A propos de Century 21 Real Estate Alliance- Century 21 Real Estate Alliance Group is the largestCentury 21 brokerage in California powered by over 1500 real estate agents working from 35 bureaux throughout California. Now offering Escrow and Lending services specializing insolutions-based lending

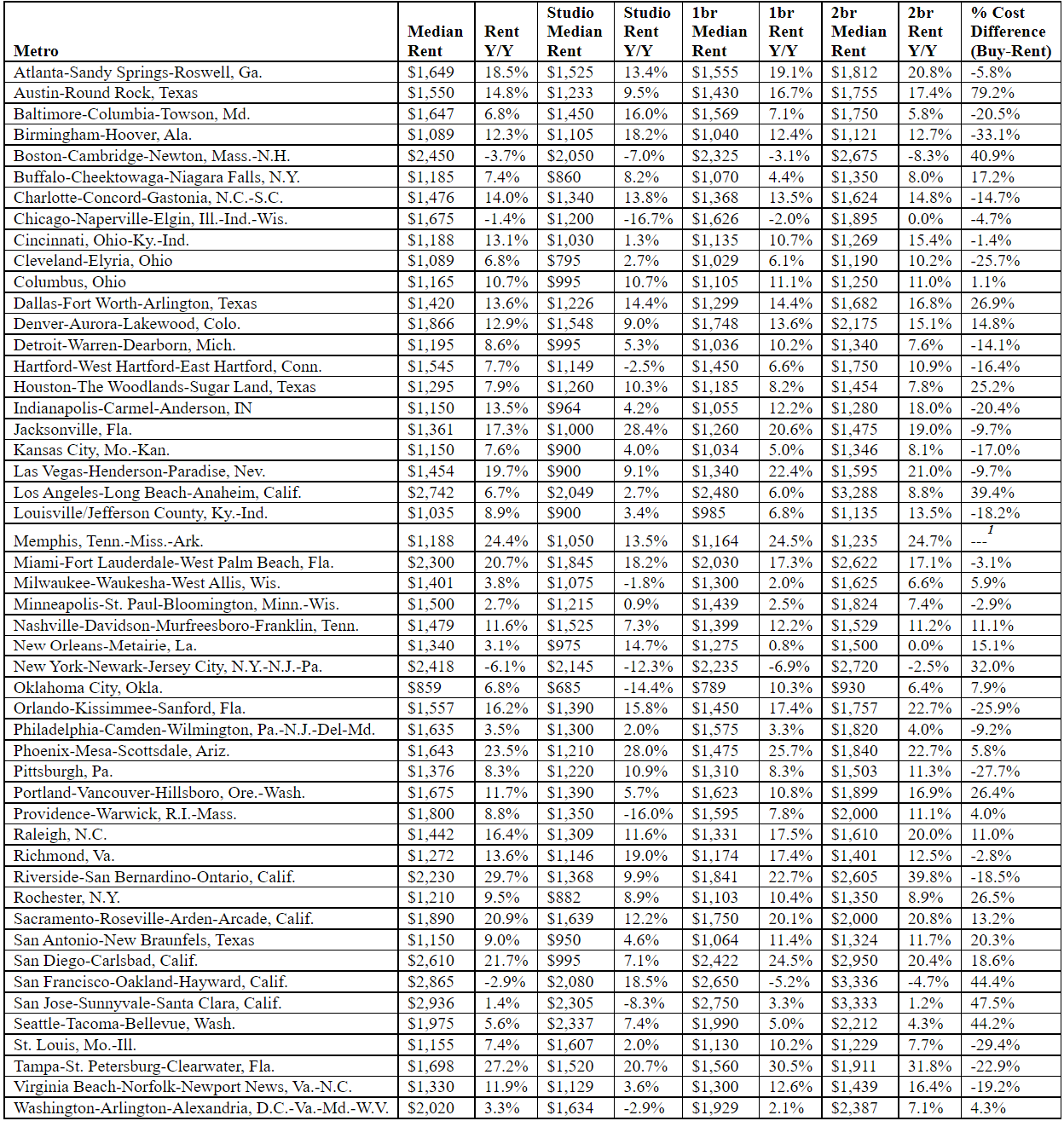

Le U.S. median rental price grew 9.8% year-over-year to $1,607 – 15.5% higher than monthly starter domicile payments in 24 of the 50 largest U.S. metros

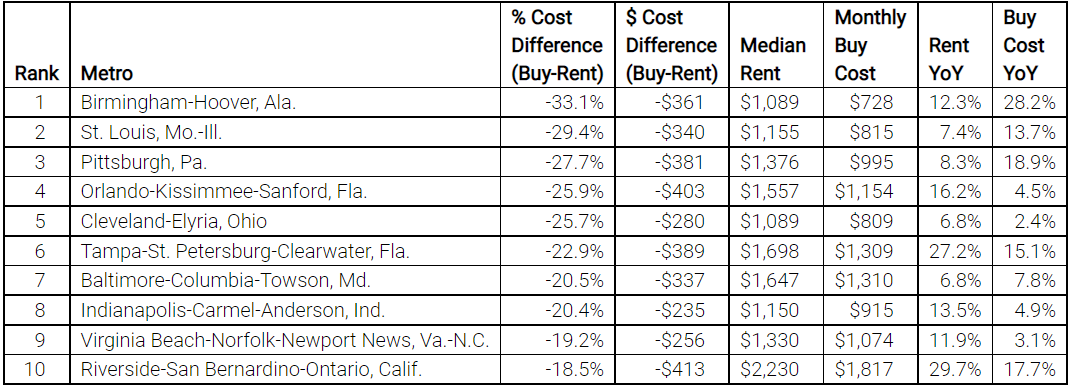

SANTA CLARA, Calif., – As rents continue to hit new highs and hypothèque rates remain low, buying a starter domicile now costs less per month than renting a similar-sized unit in 24 of the 50 largest U.S. metros, according to the Realtor.com® Monthly Rental Report released today. The top markets where it’s more affordable to buy a starter domicile versus rent one include: Birmingham, Ala. (33.1% lower), St. Louis, Mo. (29.4% lower), Pittsburgh (27.7% lower), Orlando (25.9% lower) and Cleveland (25.7% lower).

Nationally, rents continued rising at an unusually fast pace in July, up 9.8% over last year and 12.2% since 2019. All unit sizes tracked by Realtor.com® posted rent gains and hit new highs: Two-bedrooms at $1,802 (+10.9%), one-bedrooms at $1,495 (+9.5%) and studios at $1,315 (+5.6%).

“Rents hit new highs in 40 of the 50 largest U.S. metros this July and grew at an almost double-digit pace – the fastest yearly rate we’ve seen in the last 18 months,” said Realtor.com® Chief Economist Danielle Hale. “Sky-high rents and historically low interest rates have made the monthly cost to buy a starter domicile lower than renting one in nearly half the markets across the U.S. While this is good news for first-time acheteurs in these metros, there are plenty of other factors to consider when deciding whether to become a homeowner, including making sure it’s the right time for you and your family. But if the monthly costs have been holding you back, data suggests it’s worth exploring in many markets, and although it’s still hard to find entry-level homes, we are seeing more smaller homes coming on the market.”

Hale added, many of July’s highest rent gains were seen in secondary markets where rental demand has exploded during COVID, driven in part by remote work enabling employees to escape crowded, expensive big cities – at least temporarily. With the future of remote work uncertain for many Americans, first-time homebuyers saw less of a frenzy than renters in a number of July’s highest-priced rental markets. This has helped keep monthly starter domicile costs an average 15.5% ($216) lower than rents in nearly half of the 50 largest U.S. metros. (See methodology below.)

First-time homebuying is relatively more affordable in hot rental markets

In the top 10 metros that favored first-time homebuying over renting in July, monthly starter domicile payments were an average 24.3% lower than rents, driven in part by lower median listing prices ($192,000) than the national average ($297,000). The types of starter homes for sale also play a key role in monthly payments, with active inventory in these buyer-friendly metros including nearly two times the share of single-family starter homes (56.1%) than in condo-heavy markets that favor renting.

In July, the top 10 markets that favored buying over renting were: Birmingham, Ala. (33.1% lower), St. Louis, Mo. (29.4% lower), Pittsburgh (27.7% lower), Orlando (25.9% lower), Cleveland (25.7% lower), Tampa (22.9% lower), Baltimore (20.5% lower), Indianapolis (20.4% lower), Virginia Beach (19.2% lower) and Riverside, Calif. (18.5% lower).

Many of these metros also posted sizeable rent gains over last year in July, led by Riverside (+29.7%), where the median rental price of $2,230 was 18.5% ($413) higher than starter domicile payments, at $1,817 per month. Even with the surge in prices, Riverside rents were relatively lower than in nearby Los Angeles ($2,742), making the metro an attractive option to big city renters looking to save during COVID. Compared to Los Angeles, first-time homebuyers in Riverside saw 51.5% lower asking prices and nearly three times the share of single-family starter homes, at 75.1% of entry-level inventory in July.

Renting beats out buying in big tech cities with rents yet to recover from COVID

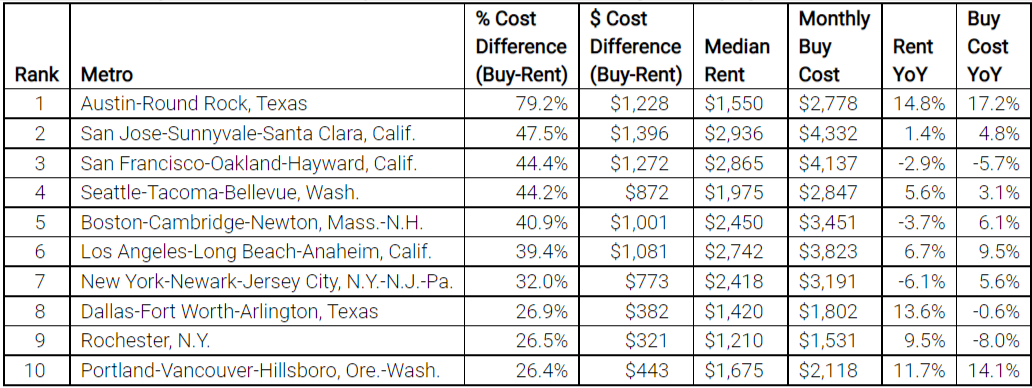

Typically some of the nation’s most expensive housing markets, big tech hubs largely favored renting over buying a starter domicile in July, partly attributed to higher condo HOA fees. Among 0-2 bedroom homes in these top 10 cities, over seven-in-ten (71%) were condos, on average, compared to 58% nationwide, while median HOA fees of $334 among homes that had this fee were 27% higher than the U.S. median ($263).

Seven of the top 10 markets where monthly starter domicile costs were higher than rents are tech-heavy areas, including: Austin, at 79.2% higher; San Jose, at 47.5% higher; San Francisco, at 44.4% higher; Seattle, at 44.2% higher; Boston, at 40.9% higher; Los Angeles at 39.4% higher; and New York, at 32.0% higher.

While rental prices have surpassed pre-COVID levels in the majority of U.S. markets, rents in many of the biggest tech cities have yet to catch up to historical peaks. Among the 50 largest U.S. markets, the only four where rents declined from last year in July were all big tech hubs: New York (-6.1%), Boston (-3.7%), San Francisco (-2.9%) and Chicago (-1.4%).

Leading the list of metros that favor renting by a wide margin, at $1,228 higher monthly starter domicile costs than rents, Austin is currently one of the nation’s most competitive housing markets. While costs like median HOA fees are relatively lower in Austin compared to other big tech cities, at $104 versus $1,222 in New York, first-time homebuyers are competing for limited affordable options, with 0-2 bedroom domicile inventory down 59% year-over-year and prices up 17.5% to a median $431,000 in July.

“Emerging tech hubs like Austin have seen a surge in housing demand in recent years as more Silicon Valley companies have opened or expanded bureaux in these areas. Relocating employees, including many millennials, can see their housing dollars go much further, with rental costs roughly half as high as in San Francisco and San Jose and starter domicile costs more than a third lower. With growth expected to continue in Austin, there’s a premium on real estate, but California transplants may find that relative affordability creates first-time homebuying opportunities,” Hale said.

Realtor.com®July 2021 Rental Data – Top 10 Markets that Favor Buying Over Renting

Realtor.com®July 2021 Rental Data – Top 10 Markets that Favor Renting Over Buying

Realtor.com®July 2021 Rental Data – 50 Largest Metropolitan Areas

Methodology

Rental data as of July 2021. Rental units include apartment communities as well as private rentals (condos, townhomes, single-family homes). All units were studio, 1-bedroom, or 2-bedroom units. National rents were calculated by averaging the medians of the 50 largest metropolitan areas.

The monthly cost of buying a domicile was calculated by averaging the median listing prices of studio, 1-bed, and 2-bed homes, weighted by the number of listings, in each housing market. Memphis for sale data was excluded while inventory data is under review. Monthly buying costs assume a 5% down payment, with a hypothèque rate of 2.87%, and include taxes, insurance and HOA fees. Typical market-level monthly HOA fees were included in the overall monthly cost of buying, and the median was not conditional on the presence of an HOA fee. This means that the typical HOA fee included reflects both the fees themselves as well as the prevalence of HOA fees in the cost of local starter homes. All else equal, areas where more homes have HOA fees will reflect a higher HOA fee inclusion.

Realtor.com® makes buying, selling, renting and living in homes easier and more rewarding for everyone. Realtor.com® pioneered the world of digital real estate more than 20 years ago, and today through its website and mobile apps is a trusted source for the information, tools and professional expertise that help people move confidently through every step of their domicile journey. Using proprietary data science and machine learning technology, Realtor.com® pairs acheteurs et vendeurs with local agents in their market, helping take the guesswork out of buying and selling a domicile. For professionals, Realtor.com® is a trusted provider of consumer connections and branding solutions that help them succeed in today’s on-demand world. Realtor.com® is operated by News Corp [Nasdaq: NWS, NWSA] [ASX: NWS, NWSLV] subsidiary Move, Inc. under a perpetual license from the National Association of REALTORS®. For more information, visit Realtor.com.

CHICAGO – (July 20, 2021) — ShowingTime, the residential real estate industry’s leading showing management and market stats technology provider, found that showing activity slowed during June compared to prior months, but remained hyperactive during the first few days listings go on the market in cities across the country.

According to the ShowingTime Showing Index®, 64 markets still averaged double-digit showings per listing during the month, led again by Seattle and Denver. That was down almost half from May, when 113 markets averaged double-digit showings per listing, and down from a very busy April when 146 markets were in double digits.

“Buyer demand remains healthy,” said ShowingTime President Michael Lane. “Showing traffic is still above last year’s levels – other than in the Northeast, where it is down 3 percent from last year – though we saw a quick month-to-month drop in the number of showings per listing in June, showing an uncharacteristically rapid slowdown in real estate demand coming into the summer. This is likely to cause an increase in inventory levels in the coming months and ease the upward pressure on real estate prices that has pushed them to historic highs over the last 12 months.”

Though the volume of showings declined from prior months, the first five days listings are active remain critical for acheteurs, when showing calendars tend to fill up quickly. Listings in Riverside and Bakersfield, Calif., Buffalo and Rochester, N.Y., Los Angeles, Raleigh, N.C., and Grand Rapids, Mich., each averaged more than 30 showings just in the first five days.

Buyer demand remained strong enough in June to drive year-over-year jumps in showing traffic in the South (20.5 percent), the West (14.4 percent) and the Midwest (14.1 percent), leading to a 7.8 percent jump year over year in activity throughout the U.S. overall. The Northeast Region, however, saw a drop of 3.2 percent, the first drop in showing activity in any region since April 2020 when real estate continued to grapple with the effects of the pandemic.

The ShowingTime Showing Index is compiled using data from more than six million property showings scheduled across the country each month on listings using ShowingTime products and services. The Showing Index tracks the average number of appointments received on active listings during the month.

ShowingTime is the residential real estate industry’s leading showing management and market stats technology provider, with more than 1.5 million active listings subscribed to its services. Its products are used in 370 MLSs representing 1.4 million real estate professionals across the U.S. and Canada. Contact us at research@showingtime.com.

More than 70% who bought a domicile in the last year feel it was a good decision and nearly half wish they had moved sooner

SANTA CLARA, Calif., May 26, 2021 — Despite the frenzied nature of today’s housing market, prompting conversations à propos de buyer’s remorse, more than two-thirds of pandemic homebuyers have found happiness in their new domicile, according to a new Realtor.com® survey released today. Those surveyed say their new domicile better fits their family’s needs and wish they moved sooner.

Realtor.com® surveyed 1,000 homeowners who purchased a new domicile during the last 12 months between March 26 – April 7 via HarrisX. In the face of the last year’s obstacles, including a competitive housing market and limitations on open houses and showings, 71% of those surveyed feel buying was a good decision and 75% say their new domicile meets their needs.

“Most of us spent more time at home during the pandemic than ever before. So it’s no surprise that it changed what many people want from their homes and neighborhoods, and created a greater sense of urgency to find a domicile that satisfied those needs,” said George Ratiu, senior economist, Realtor.com®. “With the number of available homes for sale in short supply, acheteurs didn’t have many choices over the past year, or a lot of time to consider their options in a very competitive market. However, as our survey shows, pandemic acheteurs generally feel good à propos de the choices they made, and while the homebuying process itself is stressful, new homeowners feel their new homes meet their needs and do not regret the choices they made.”

More than half (55%) of the homeowners surveyed found a new domicile that is exactly what they need for working or schooling from domicile.

However, even more are satisfied with elements of their new domicile that are important to everyday life during and after the pandemic. When asked how they feel à propos de their domicile, neighborhood and area, more than 70% of new homeowners report feeling “happy.” Based on their reported satisfaction, 45% of new homeowners wish they had moved sooner, while only 19% say they should have waited.

Not rushed, on-budget, and no regrets

Three-quarters of the new homeowners surveyed were planning to buy prior to the onset of COVID, while the remaining quarter decided to purchase because of the pandemic. With pandemic acheteurs in many régions having to do more of their domicile search virtually and the need to make quick decisions, buyer’s remorse could have been a common outcome.

Despite the frenzy, acheteurs have no regrets when it comes to how quickly they made their purchase and how much they paid. Less than one-third said they wished they’d spent more time on their domicile search before buying and nearly half (48%) did not feel rushed or pressured into making a domicile-buying decision. They also didn’t feel as if they overpaid, with 61% of those surveyed reporting that the purchase price of their new domicile was either at or under their original budget.

Prioritization is key in a fast-paced market

With a lack of available inventory and homes selling at record pace and prices, acheteurs not only need to move quickly, but they have to be prepared to compromise. Trade-offs are an inevitable part of the process, especially for first-time buyers who don’t have equity from a previous domicile sale to use as a down payment.

“Buying a domicile is the biggest financial decision most people make and, while there’s pressure to move more quickly, especially today, it’s not a decision you want to make lightly,” said Lexie Holbert, domicile and living expert at Realtor.com®. “Nothing in life is perfect, and a new domicile is no exception, so compromises are always part of the buying process. The best place to start is with a budget, and from there you can prioritize what’s important to you. Is it square footage, number of bedrooms, outdoor space or location? Once you have an idea of what’s most important, you’re ready to make confident decisions.”

Accueil shoppers who use Realtor.com® can find tips on how to compete in today’s market on its News & Insights site et Accueil Made blog. Users also can download the Realtor.com® Real Estate app to sign up for custom search alerts that notify them à propos de new listings in their desired area and price drops on saved homes so they know as soon as a domicile that matches their criteria hits the market.

Methodology: Realtor.com® commissioned HarrisX to conduct a national survey of consumers. This survey was conducted online within the United States from March 26 – April 7, 2021. The survey was conducted among 3,998 adults by HarrisX. The sampling margin of error of this poll is plus or minus 1.6 percentage points. The results reflect a nationally representative sample of adults. Results were weighted for age, gender, region, race/ethnicity, and income where necessary to align them with their actual proportions in the population. In addition to the general population, an oversample was collected for new homeowners. The oversample was weighted to align with the original sample. There are 1,000 new owners who bought a domicile in the last 12 months with a margin of error of plus or minus 3.1 percentage points.

The 2021 spring housing market can be summed up to two extremes better suited for a primetime TV medical drama than an economic snapshot: the vendeurs market is on steroids, while the acheteurs markets are on life support.

Why so extreme?

Real estate laws of supply and demand dictate that rising demand reduces the number of homes for sale and increase prices. Higher prices then motivate vendeurs to sell, opening greater supplies of inventories and reducing the pressure on prices. Moderated prices and more homes for sale encourage acheteurs to buy, and sales increase until supply and demand start their familiar dance all over again.

That’s how things are supposed to work.

Except, moving into the spring 2021 housing market, they aren’t working that way at all. Soaring prices and starving inventories aren’t motivating enough vendeurs to sell, nor are they discouraging many acheteurs from buying. So, we’re left with a pair of extremes, whose forces are stronger than supply and demand, and twisting housing markets out of shape.

Fear Worsened the Inventory Drought

Even before the COVID-19 pandemic and current recession, the housing market was facing a substantial supply shortage. Afraid of missing out on the lowest hypothèque interest rates in a generation, extraordinary numbers of millennial first-time acheteurs jumped into the markets in the first weeks of the pandemic’s arrival in March 2020.

However, millions of vendeurs delayed listing their homes at the launch of the spring 2020 sales season. By July, high demand and low supplies drove sales prices to an all-time high, and inventory levels plunged 21.1% below 2019 levels, marking 14 straight months of year-over-year declines.

Inventories Are Still Disastrously Low

Fast forward to the end of February 2021, housing inventory was a record 29.5% lower than a year earlier. Acheteurs quickly consumed the new listings, and time on the market fell to 20 days for a domicile to go from listing to contract, an all-time low.

At the end of March, total housing inventory amounted to 1.07 million units, up 3.9% from February but still down 28.2% from one year ago. Unsold inventory stayed at a 2.1-month supply, marginally up from February’s 2.0-month supply and down from the 3.3-month supply recorded in March 2020. Inventory numbers continue to represent near-historic lows since NAR first began tracking the single-family domicile supply in 1982. In fact, according to the National Association of Realtors, the U.S. housing market is short à propos de 3 million available homes.

Looking beyond the spring 2021 housing market itself, a more enduring problem is the chronic underproduction of new homes. For five decades, America’s supply of entry-level homes has declined. Production of entry-level construction fell from 418,000 units per year in the late 1970s to 65,000 in 2020. According to NAR’s Lawrence Yun, new-domicile underproduction is the chief cause of today’s inventory shortage. Freddie Mac’s chief economist, Sam Khater, agrees.

“Simply put, we must build more single-family entry-level housing to address this shortage, which has strong implications for the wealth, health, and stability of American communities,” Khater says.

Typically in a recessionary time (such as the pandemic), housing demand declines and supply rises, causing inventory to rise above the long-term trend. Khater believes the main driver of the housing shortfall to be the long-term decline in the construction of single-family homes.

When falling rates led to higher demand, supplies could not keep up, and by late 2020, prices soared at a double-digit pace. Shortages of affordable homes brought the pandemic sales boom to a halt. Sales fell 6.6% from January 2021 to February, and supplies did not increase during February, a month when vendeurs traditionally begin to list their homes for the spring sales season.

Rates and Prices Will Slowly Rise During the Year

So far, the spring 2021 housing market has been a mixed bag. During the first quarter of 2021, rates on a 30-year fixed-rate hypothèque stayed below 3% percent until the first week of March. By April 1, however, they reached 3.18%, which lowered the house-buying power of consumers enough to cost 55,600 potential domicile sales, according to First American’s chief economist Mark Fleming. Freddie Mac’s forecasters expect rates to continue to rise slowly and reach an average of 3.4% in the fourth quarter of 2021, as the economy slowly recovers from the pandemic.

What We Can Expect Moving Forward

As long as the economic outlook post-COVID is optimistic, interest rates should go higher. Despite the nation’s continued economic uncertainty, demand drivers will continue in 2021, and rates, though starting to increase, will still remain very low. A gradual return to normalcy will raise incomes, and lenders will discontinue some of their pandemic-era restrictions. More millennials and Gen Xers will enter the market, especially with those low rates.

Freddie Mac’s forecasters expect the rate on a 30-year fixed hypothèque rate to average 3.4% by the fourth quarter of 2021, rising to 3.8% in the fourth quarter of 2022.

Fannie Mae forecasts that housing starts will rise 17% by the end of the second quarter over last year’s poor performance, then 4.7% in the third quarter. The massive shortfall in unsold inventory will continue, especially for affordable starter homes. Supplies are at record low levels this spring, and they will not normalize until new construction can meet the demands of a growing population.

For now, the spring 2021 housing market is just one snapshot of many in a tale that is poised to get worse before it gets better.

RETechnology.com – Steve Cook is the editor of the Down Payment Report and provides public relations consulting services to leading companies and non-profits in residential real estate and housing finance. He has been vice president of public affairs for the National Association of Realtors, senior vice president of Edelman Worldwide and press secretary to two members of Congress.